ESG Reporting Framework Guide: CSRD, GRI, SASB, and TCFD Explained (2026)

schema: | { “@context”: “https://schema.org”, “@graph”: [ { “@type”: “Article”, “headline”: “ESG Reporting Framework Guide: CSRD, GRI, SASB, and TCFD Explained (2026)”, “description”: “Complete guide to ESG reporting frameworks including CSRD, GRI, SASB, TCFD, and ISSB standards. Learn requirements, differences, and implementation strategies for 2026.”, “image”: “https://bato.com.np/assets/images/esg-frameworks-cover.jpg”, “datePublished”: “2026-02-18”, “dateModified”: “2026-02-21”, “author”: { “@type”: “Person”, “name”: “Laura Bennett” }, “publisher”: { “@type”: “Organization”, “name”: “BATO - Business Audit & Tax Organization”, “logo”: { “@type”: “ImageObject”, “url”: “https://bato.com.np/assets/images/logo.png” } } } ] }

Environmental, Social, and Governance (ESG) reporting has evolved from voluntary disclosure to mandatory requirement in many jurisdictions. This comprehensive guide explains major ESG frameworks and how to navigate the complex reporting landscape in 2026.

- The ESG Reporting Landscape

- Major ESG Reporting Frameworks

- 1. EU Corporate Sustainability Reporting Directive (CSRD)

- 2. Global Reporting Initiative (GRI)

- 3. Sustainability Accounting Standards Board (SASB)

- 4. Task Force on Climate-related Financial Disclosures (TCFD)

- 5. International Sustainability Standards Board (ISSB)

- 6. SEC Climate Disclosure Rule (Proposed)

- Choosing the Right Framework

- Implementation Strategy

- Industry-Specific Guidance

- Common Challenges and Solutions

- Best Practices

- Future Outlook

- Conclusion

- Resources

The ESG Reporting Landscape

Why ESG Reporting Matters

Stakeholder Pressures:

- Investors demanding transparency

- Customers prioritizing sustainable companies

- Employees seeking purpose-driven employers

- Regulators mandating disclosure

- Supply chain requirements cascading downstream

Business Benefits:

- Risk Management: Identify and mitigate ESG risks

- Capital Access: Lower cost of capital

- Reputation: Enhanced brand value

- Operational Efficiency: Cost savings through sustainability

- Talent Attraction: Appeal to values-driven workforce

Market Realities (2026):

- $50+ trillion in ESG-related assets under management

- 90% of S&P 500 companies publish sustainability reports

- Mandatory reporting expanding globally

- Integration with financial reporting increasing

Evolution of ESG Standards

Historical Development:

2000: Global Reporting Initiative (GRI) launched

2006: UN Principles for Responsible Investment

2011: Sustainability Accounting Standards Board (SASB) founded

2015: Task Force on Climate-related Financial Disclosures (TCFD)

2021: International Sustainability Standards Board (ISSB) created

2023: EU Corporate Sustainability Reporting Directive (CSRD) effective

2024: California climate disclosure laws (SB 253/261)

2026: SEC climate rule implementation (if finalized)

Current Landscape:

- Fragmentation gradually reducing

- Convergence around core frameworks

- Mandatory regimes expanding

- Assurance requirements increasing

Major ESG Reporting Frameworks

1. EU Corporate Sustainability Reporting Directive (CSRD)

Overview: The CSRD is the most comprehensive mandatory ESG reporting regime, affecting thousands of EU and non-EU companies.

Effective Dates:

- 2024: Large EU public-interest entities (>500 employees)

- 2025: Other large EU companies

- 2026: Listed SMEs (small and medium enterprises)

- 2028:Non-EU companies with significant EU operations

Scope and Applicability:

EU Companies Covered:

- Large undertakings meeting 2 of 3 criteria:

- €25M+ balance sheet

- €50M+ net turnover

- 250+ employees on average

- All listed companies (except micro-enterprises)

- Parent companies of large groups

Non-EU Companies: Must comply if:

- €150M+ EU turnover

- At least one EU subsidiary or branch meeting thresholds

Estimated Impact: ~50,000 companies globally

Key Requirements:

1. Double Materiality Assessment

- Impact Materiality: How company affects people/planet

- Financial Materiality: How sustainability matters affect financial performance

- Report on both perspectives

2. European Sustainability Reporting Standards (ESRS) Mandatory disclosure across:

- ESRS 1: General Requirements

- ESRS 2: General Disclosures

- ESRS E1-E5: Environmental (climate, pollution, water, biodiversity, circular economy)

- ESRS S1-S4: Social (workforce, workers in value chain, communities, consumers)

- ESRS G1: Governance

3. Detailed Disclosures Required:

- Strategy: Business model, sustainability strategy, resilience

- Governance: Roles, responsibilities, incentives

- Impacts, Risks, Opportunities (IROs): Assessment and management

- Metrics and Targets: KPIs, progress tracking, forward-looking targets

4. Digital Reporting:

- Must be included in management report

- Tagged using European Single Electronic Format (ESEF)

- Machine-readable (XBRL taxonomy)

5. Limited Assurance Required:

- Mandatory limited assurance from 2024

- Reasonable assurance by 2028

- Independent third-party verification

Penalties and Enforcement:

- Member states determine penalties

- Must be “effective, proportionate, and dissuasive”

- Potential sanctions include fines, director liability

Comparison to Previous NFRD:

Non-Financial Reporting Directive (NFRD):

- ~11,000 companies

- High-level, principles-based

- No specific standards

- No assurance requirement

CSRD:

- ~50,000 companies

- Detailed, prescriptive ESRS

- Mandatory standards

- Independent assurance

- Digital, machine-readable format

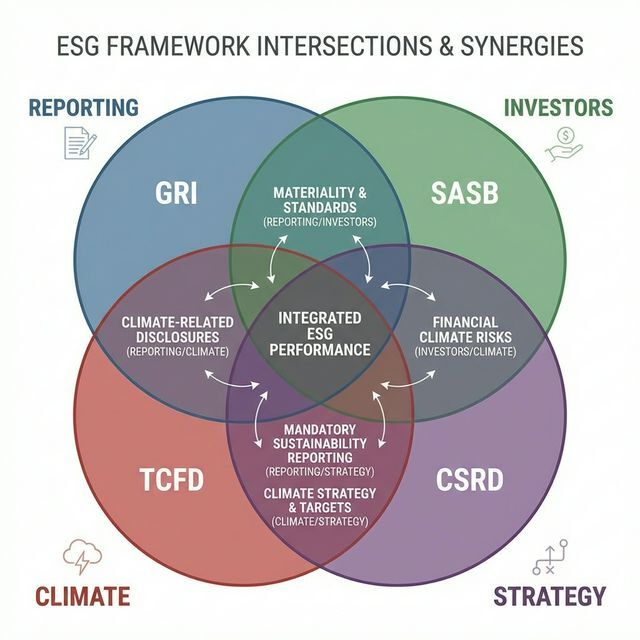

2. Global Reporting Initiative (GRI)

Overview: The most widely used voluntary sustainability reporting framework globally, established in 2000.

Usage Statistics (2026):

- 15,000+ organizations use GRI

- Recognized in 90+ countries

- Referenced by many mandatory frameworks

- Multi-stakeholder governance

Framework Structure:

Universal Standards (Apply to All):

- GRI 1: Foundation

- GRI 2: General Disclosures (organization profile, activities, governance, stakeholder engagement)

- GRI 3: Material Topics (determination process, topic list, management approach)

Topic-Specific Standards:

Economic (200 Series):

- GRI 201: Economic Performance

- GRI 202: Market Presence

- GRI 203: Indirect Economic Impacts

- GRI 204: Procurement Practices

- GRI 205: Anti-corruption

- GRI 206: Anti-competitive Behavior

- GRI 207: Tax (added 2019)

Environmental (300 Series):

- GRI 301: Materials

- GRI 302: Energy

- GRI 303: Water and Effluents

- GRI 304: Biodiversity

- GRI 305: Emissions

- GRI 306: Waste

- GRI 307: Environmental Compliance

- GRI 308: Supplier Environmental Assessment

Social (400 Series):

- GRI 401: Employment

- GRI 402: Labor/Management Relations

- GRI 403: Occupational Health and Safety

- GRI 404: Training and Education

- GRI 405: Diversity and Equal Opportunity

- GRI 406: Non-discrimination

- GRI 407-411: Labor practices

- GRI 413: Local Communities

- GRI 414: Supplier Social Assessment

- GRI 415: Public Policy

- GRI 416-418: Product responsibility

Reporting Principles:

Report Content:

- Stakeholder Inclusiveness: Respond to stakeholder expectations

- Sustainability Context: Present performance in broader sustainability context

- Materiality: Reflect significant economic, environmental, and social impacts

- Completeness: Sufficient coverage to enable stakeholders to assess performance

Report Quality:

- Accuracy: Information must be correct and detailed

- Balance: Both positive and negative results

- Clarity: Information accessible and understandable

- Comparability: Consistent over time and against others

- Reliability: Traceable and verifiable

- Timeliness: Report on regular schedule

Materiality Assessment Process:

- Identify potential impacts

- Assess significance (severity + likelihood)

- Prioritize most significant

- Validate with stakeholders

- Report material topics

Compliance Levels:

- GRI-referenced: Use some GRI disclosures

- In accordance: Full compliance with standards

- Core: Essential elements

- Comprehensive: All applicable disclosures

3. Sustainability Accounting Standards Board (SASB)

Overview: Industry-specific standards focused on financially material sustainability information for investors.

Key Characteristics:

- Investor-focused: Designed for 10-K/annual report integration

- Financially material: Focus on financial performance impacts

- Industry-specific: 77 standards across 11 sectors

11 Sectors Covered:

- Consumer Goods

- Extractives & Minerals Processing

- Financials

- Food & Beverage

- Health Care

- Infrastructure

- Renewable Resources & Alternative Energy

- Resource Transformation

- Services

- Technology & Communications

- Transportation

26 ESG Issues Tracked:

- Environment: GHG emissions, air quality, energy, water, waste, ecological impacts

- Social Capital: Human rights, customer privacy, data security, fair marketing

- Human Capital: Labor practices, employee health & safety, engagement, diversity

- Business Model: Product design, lifecycle management, supply chain, materials sourcing

- Leadership & Governance: Business ethics, competitive behavior, regulatory capture, critical incident management, systemic risk

Standard Structure:

Each industry standard includes:

- Topic: Sustainability issue

- Metric: Specific KPI to track

- Unit of Measure: Standardized format

- Category: Accounting metric type

Example: Software & IT Services Industry

Topic: Data Privacy & Freedom of Expression

Metrics:

- (1) Number of self-regulatory or government actions against databreaches/privacy violations

- (2) Total amount of monetary losses as result of legal proceedings

Topic: Employee Engagement & Diversity

Metrics:

- Percentage of gender and racial/ethnic group representation:

(1) Management (2) Technical staff (3) All other employees

Implementation:

- Identify your SASB industry classification

- Review the industry standard

- Collect data for required metrics

- Integrate into investor communications

- Disclose in 10-K, 20-F, or sustainability report

Notable Features:

- Concise (average 10 pages per industry)

- Quantitative metrics emphasized

- Decision-useful for investors

- Benchmarkable across peers

4. Task Force on Climate-related Financial Disclosures (TCFD)

Overview: Framework focused specifically on climate-related financial risks and opportunities, established by Financial Stability Board in 2015.

Adoption:

- 4,000+ organizations support TCFD

- Mandatory in UK, New Zealand, Switzerland

- Referenced in SEC proposed climate rule

- Integrated into ISSB standards (2024)

Four Pillars:

1. Governance Disclose organization’s governance around climate risks/opportunities:

- Board oversight of climate issues

- Management’s role in assessing and managing

- Integration into overall strategy

- Skills and competencies

2. Strategy Actual and potential climate impacts on business, strategy, financial planning:

- Climate-related risks and opportunities over short/medium/long-term

- Impact on business, strategy, and financial planning

- Resilience of strategy under different climate scenarios

- Transition and physical risks identified

3. Risk Management How organization identifies, assesses, and manages climate risks:

- Processes for identifying climate risks

- Processes for managing climate risks

- Integration into overall risk management

4. Metrics and Targets Metrics and targets used to assess and manage relevant climate risks/opportunities:

- Scope 1 Emissions: Direct emissions from owned/controlled sources

- Scope 2 Emissions: Indirect emissions from purchased electricity, heat, steam

- Scope 3 Emissions: All other indirect emissions in value chain

- Climate-related risks exposure

- Opportunities pursued

- Capital deployment

- Internal carbon price (if used)

- Compensation linkage

- Targets and performance

Scenario Analysis: Key differentiator of TCFD:

- Test strategy resilience under different climate futures

- Typical scenarios:

- 2°C or lower: Paris Agreement aligned

- Business as usual: Current trajectory (3-4°C)

- Other relevant scenarios: Physical risk-focused

Example Scenario Inputs:

- Carbon pricing assumptions

- Energy price evolution

- Technology costs and adoption

- Policy and regulatory changes

- Physical climate parameters

Implementation Challenges:

- Scenario analysis complexity

- Scope 3 emissions measurement

- Forward-looking vs. historical disclosure

- Data availability and quality

5. International Sustainability Standards Board (ISSB)

Overview: New global baseline for sustainability disclosure focused on enterprise value, established by IFRS Foundation in 2021.

Mission: Create globally accepted sustainability disclosure standards that complement IFRS Accounting Standards.

IFRS Sustainability Disclosure Standards:

IFRS S1: General Requirements (effective 2024)

- Core framework for sustainability-related financial disclosures

- Four-pillar structure aligned with TCFD:

- Governance

- Strategy

- Risk management

- Metrics and targets

- Single materiality perspective (financial materiality)

- Connected to financial statements

IFRS S2: Climate-related Disclosures (effective 2024)

- Climate-specific requirements

- Scope 1, 2, and 3 emissions (with transition relief)

- Climate resilience and scenario analysis

- Industry-based metrics (incorporating SASB)

Key Features:

- Enterprise value focus: Investor-oriented

- Global baseline: Intended for worldwide adoption

- Interoperability: Designed to work with regional requirements

- Scalability: Proportionate implementation

- Connectivity: Linked to financial statements

Relationship to Other Frameworks:

- Built on TCFD: Four-pillar structure

- Incorporates SASB: Industry-based metrics

- Compatible with GRI: Can report both (GRI = stakeholders, ISSB = investors)

- Basis for CSRD: EU ESRS builds on ISSB

Adoption Status (2026):

- UK: Mandatory for certain companies

- Canada: Adoption planned

- Australia: Aligned standards developed

- Singapore: Voluntary adoption supported

- Japan: Considering adoption

- US SEC: Watching development

6. SEC Climate Disclosure Rule (Proposed)

Status as of 2026: Final rule implementation phase (if adopted as proposed).

Proposed Requirements:

Scope 1 & 2 GHG Emissions:

- Large accelerated filers and accelerated filers

- If material, or if target/goal set

- Phased implementation

Scope 3 GHG Emissions:

- Only if material

- Safe harbor for liability

- Many companies may opt not to disclose

Climate-Related Risks:

- Material risks affecting strategy, business model, outlook

- Physical risks (acute and chronic)

- Transition risks (policy, legal, technology, market, reputation)

Governance:

- Board oversight

- Management role

- Expertise and skills

Risk Management:

- Processes for identifying, assessing, managing climate risks

- Integration with overall risk management

Financial Statement Impacts:

- Expenditure impacts (expensed and capitalized)

- Impacts on financial estimates and assumptions

- Separate line items if exceeding 1% threshold

Targets and Goals:- Scope 1, 2, 3 targets if set

- Transition plans

- Use of carbon offsets/RECs

Assurance:

- Limited assurance required (after phase-in)

- Reasonable assurance in later years

Expected Timeline:

- Phased approach over 3-4 years

- Large companies first

- Smaller companies delayed implementation

Choosing the Right Framework

Framework Selector

If you are:

Required to report under CSRD:

- Primary: ESRS (mandatory)

- Can also use: GRI for voluntary expanded disclosure

- Include: TCFD pillars (embedded in ESRS)

Public company, investor-focused:

- Primary: ISSB S1 & S2 (or SASB if reporting pre-ISSB)

- Include: TCFD recommendations

- Consider: SEC requirements if US-listed

Voluntary reporter, broad stakeholders:

- Primary: GRI Standards

- Consider adding: SASB for investor audience

- Include: TCFD climate disclosures

Climate focus specifically:

- Use: TCFD framework

- Expanding to: ISSB S2

- Include: SASB climate metrics for your industry

Multi-Framework Approach

Many companies use combination:

Common Combination:

- GRI: Comprehensive sustainability report (stakeholders)

- SASB: Industry-specific metrics in 10-K (investors)

- TCFD: Climate section of sustainability report

- Local: Comply with mandatory requirements (CSRD, SEC, etc.)

Benefits:

- Serve different audiences

- More comprehensive coverage

- Demonstrate leadership

- Prepare for evolving mandates

Challenges:

- Resource intensive

- Potential duplication

- Complexity in management

- Need for robust data systems

Implementation Strategy

Phase 1: Assessment and Planning (Months 1-3)

1. Understand Requirements

- Identify applicable frameworks

- Determine mandatory vs. voluntary

- Assess timelines and deadlines

- Review industry peers’ practices

2. Gap Analysis

- Current state of ESG data collection

- Identify gaps vs. requirements

- Assess system and process needs

- Evaluate resource requirements

3. Stakeholder Engagement

- Internal: Board, management, operations

- External: Investors, customers, suppliers, communities

- Determine material issues

- Prioritize based on significance

4. Governance Structure

- Establish cross-functional team

- Define roles and responsibilities

- Set up reporting lines

- Create steering committee

Phase 2: Double Materiality Assessment (Months 3-5)

Step 1: Identify Impacts, Risks, and Opportunities

- Brainstorm ESG issues relevant to your business

- Review framework guidance

- Consider value chain (upstream/downstream)

- Catalogue: ~30-50 potential topics

Step 2: Assess Impact Materiality For each topic:

- Scale of impact (how serious)

- Scope of impact (how widespread)

- Irremediable character (how hard to fix)

Step 3: Assess Financial Materiality For each topic:

- Likelihood of occurrence

- Magnitude of financial effect

- Timeframe (short/medium/long-term)

Step 4: Prioritize Create materiality matrix:

- X-axis: Financial materiality

- Y-axis: Impact materiality

- Identify topics in upper-right (material on both dimensions)

Step 5: Validate

- Review with senior management

- Validate with external stakeholders

- Document process thoroughly

- Update annually

Phase 3: Data Collection Infrastructure (Months 4-8)

1. Data Inventory

- Map existing data sources

- Identify data owners

- Document data quality

- Catalogue gaps

2. System Assessment

- Evaluate current systems capability

- Determine ESG software needs

- Integration with financial systems

- Consider: SAP Sustainability Control Tower, Workiva, Enablon, Sphera

3. Process Design

- Data collection procedures

- Quality control mechanisms

- Approval workflows

- Update frequency

4. Pilot Program

- Test with one business unit/location

- Refine processes

- Train data providers

- Scale learnings across organization

Phase 4: Metric Development (Months 6-10)

Environmental Metrics:

- GHG Emissions: Scope 1, 2, 3 (per GHG Protocol)

- Energy: Total consumption, renewable percentage

- Water: Withdrawal, consumption, regions of stress

- Waste: Total generated, diverted from landfill

- Biodiversity: Sites in protected areas, assessment conducted

Social Metrics:

- Diversity: Gender, ethnicity across levels

- Health & Safety: TRIR, LTIR, fatalities

- Training: Hours per employee, spend

- Turnover: Voluntary/involuntary rates

- Community: Investment, volunteer hours

- Human Rights: Assessments, training

Governance Metrics:

- Board Composition: Independence, diversity, tenure

- Ethics: Training completion, violations

- Cybersecurity: Incidents, response time

- Compliance: Violations, fines

- Supplier Practices: Assessments conducted, corrective actions

Setting Targets:

- Science-based (climate)

- Time-bound

- Quantifiable

- Publicly communicated

- Progress tracked and reported

Phase 5: Reporting and Disclosure (Months 10-12)

Report Structure:

Executive Summary

- CEO letter

- Key achievements

- Material topics overview

About the Company

- Business model

- Products/services

- Geographic presence

- Stakeholder engagement

Sustainability Strategy

- Vision and commitments

- Material topics and why they matter

- Alignment with UN SDGs

- Governance structure

Performance by Topic For each material topic:

- Management approach

- Specific policies

- Actions taken in reporting year

- Results and metrics

- Progress against targets

- Future plans

Data Tables

- Multi-year trending data

- Industry-specific metrics

- SASB/GRI content indexes

Assurance Statement

- Independent verification

- Scope of assurance

- Methodology

- Findings

GRI/SASB Index

- Cross-reference to framework requirements

2. Digital Reporting

- Sustainability section on website

- Interactive data visualizations

- Downloadable PDF

- XBRL tagging (if required)

3. Integration

- 10-K/Annual Report ESG section

- Proxy statement linkages

- Investor presentations

- Other corporate communications

Phase 6: Assurance (Ongoing)

Limited Assurance (Current Standard):

- Review procedures, interviews, walkthroughs

- Analytical procedures

- Limited testing

- “Nothing has come to our attention” conclusion

Reasonable Assurance (Future Direction):

- Substantive testing

- Detailed verification

- Similar to financial audit

- Positive assurance opinion

Choosing Assurance Provider:

- Big 4 Accounting Firms: Comprehensive, high credibility

- Specialized ESG Firms: Deep ESG expertise

- Engineering Firms: Technical environmental expertise

- Certification Bodies: Standards-based verification

Scope Considerations:

- All data vs. selected metrics

- Global vs. specific geographies

- Like-for-like boundaries vs. expanding

- Phased approach common

Industry-Specific Guidance

Financial Services

Material Topics:

- Climate risk in lending/investment portfolios

- Financed emissions (Scope 3)

- Sustainable finance products

- Financial inclusion

- Data privacy and cybersecurity

Key Standards:

- SASB: FN-CB, FN-IB, FN-AC (banking, investment, insurance)

- TCFD: Portfolio climate risk assessment

- CSRD: Mandatory for EU entities

Manufacturing

Material Topics:

- Scope 1 & 2 emissions from operations

- Energy efficiency and renewable energy

- Water management

- Waste and circular economy

- Supply chain labor practices

Key Standards:

- SASB: RT- industries (Resource Transformation)

- GRI: Environmental standards (300 series)

- CSRD: ESRS E1-E5 (environmental)

Technology

Material Topics:

- Data center energy use (significant)

- Product lifecycle and e-waste

- Data privacy and security

- Diversity and inclusion

- Content governance

Key Standards:

- SASB: TC-SI (Software & IT Services)

- GRI: Privacy, cybersecurity disclosures

- Specific to data centers: PUE metrics

Retail

Material Topics:

- Supply chain transparency

- Product sustainability

- Labor practices in supply chain

- Scope 3 emissions (products, shipping)

- Packaging and waste

Key Standards:

- SASB: CG-MR (Multiline and Specialty Retailers)

- GRI: Supply chain assessments

- French Duty of Vigilance law (if applicable)

Common Challenges and Solutions

Challenge 1: Data Quality and Availability

Issues:

- Manual collection processes

- Inconsistent reporting from sites

- Missing historical data

- Estimations and assumptions

Solutions:

- Invest in ESG data management software

- Automate data flows from source systems

- Establish data quality standards

- Document estimation methodologies

- Implement regular data reviews

- Build in time to improve over years

Challenge 2: Scope 3 Emissions

Issues:

- Represents 70-90% of footprint for many companies

- Requires supplier engagement

- Limited data availability

- High degree of estimation

Solutions:

- Start with spend-based methodology

- Gradually move to supplier-specific data

- Engage key suppliers systematically

- Use industry average data initially

- Platform solutions (CDP Supply Chain, etc.)

- Set supplier expectations in contracts

Challenge 3: Evolving Standards

Issues:

- Standards continue to change

- New requirements emerging

- Keeping up with updates

- Balancing consistency with improvement

Solutions:

- Monitor standard-setter announcements

- Join industry working groups

- Engage professional advisors

- Build flexibility into systems

- Document changes year-over-year

- Explain methodology changes

Challenge 4: Resource Constraints

Issues:

- Significant time investment required

- Expertise needed across topics

- Competing priorities

- Budget limitations

Solutions:

- Phased implementation approach

- Leverage external consultants selectively

- Use materiality to prioritize

- Build internal capabilities over time

- Technology to improve efficiency

- Cross-functional collaboration

Best Practices

1. Start with Strategy

Don’t just report—integrate ESG into:

- Corporate strategy

- Risk management

- Capital allocation

- Performance management

- Compensation

2. Tell Your Story

Beyond metrics:

- Explain context and challenges

- Share journey and evolution

- Highlight innovations

- Present both successes and setbacks

- Connect to business value

3. Be Transparent

Stakeholders value honesty:

- Acknowledge gaps and limitations

- Explain estimation methodologies

- Discuss challenges faced

- Show progress over time

- Don’t greenwash

4. Engage Stakeholders

Continuously:

- Investors (increasingly sophisticated)

- Employees (especially younger generations)

- Customers (purchase decisions driven by values)

- Suppliers (affected by your requirements)

- Communities (local impacts)

5. Link to Finance

Make connections clear:

- Financial impacts of ESG issues

- ESG factors in enterprise risk

- Integration in investor presentations

- Alignment with financial reporting timelines

6. Invest in Systems

Technology enablers:

- Automated data collection

- Workflow management

- Calculation engines

- Reporting outputs

- Assurance evidence

- Benchmarking capabilities

7. Build Capabilities

Develop internal expertise:

- Training programs

- Dedicated ESG roles

- Cross-functional teams

- External partnerships

- Knowledge sharing

Future Outlook

Trends for 2026-2030

Regulatory:

- Continued expansion of mandatory reporting

- Assurance requirements tightening

- Enhanced liability for misstatements

- Increased enforcement actions

Standards:

- Further consolidation around ISSB globally

- CSRD as comprehensive EU model

- US SEC rule finalization

- Baseline plus regional requirements

Technology:

- AI in data collection and analysis

- Blockchain for supply chain transparency

- IoT sensors for real-time monitoring

- Improved calculation tools

- Integrated reporting platforms

Assurance:

- Movement toward reasonable assurance

- Specialized ESG audit professionals

- Technology-enabled testing

- Real-time/continuous assurance

Integration:

- ESG within annual reports (not separate)

- Connectivity with financial statements

- Single reporting timeline

- Unified corporate reporting

Conclusion

ESG reporting in 2026 is complex but increasingly standardized. While challenges remain, frameworks are converging and best practices are emerging. Success requires strategic commitment, robust data infrastructure, and continuous improvement.

Key Takeaways:

- Mandatory reporting expanding rapidly (especially CSRD)

- Multiple frameworks serve different purposes

- Double materiality is becoming standard

- Assurance requirements increasing

- Technology investment is essential

- Start now—it takes longer than expected

- View as strategic opportunity, not just compliance

Getting Started Checklist:

- Identify applicable mandatory requirements

- Conduct double materiality assessment

- Establish governance structure

- Build data collection infrastructure

- Develop metrics and targets

- Prepare initial disclosure

- Obtain assurance

- Publish and communicate

- Monitor feedback and improve

- Keep current with evolving standards

Resources

- CSRD: EU website (ec.europa.eu)

- GRI: Global Reporting Initiative (globalreporting.org)

- SASB: SASB Standards (sasb.org, now part of IFRS Foundation)

- TCFD: Task Force on Climate-related Financial Disclosures (fsb-tcfd.org)

- ISSB: International Sustainability Standards Board (ifrs.org/groups/issb)

- CDP: Carbon Disclosure Project (cdp.net)

- UN Global Compact: Sustainability reporting resources

Related Articles

- ESG Materiality Assessment: Identifying, Prioritizing, and Reporting Material ESG Issues (2026)

- ESG Investing: What Every Institutional Investor Needs to Know in 2026

- Environmental Compliance and ESG Guide: Sustainability Regulations, Reporting Standards, and Risk Management (2024-2026)

- AI in Accounting & Audit: The Practical 2026 Guide