Complete Guide to Audit Requirements Worldwide (2026)

schema: | { “@context”: “https://schema.org”, “@graph”: [ { “@type”: “Article”, “headline”: “Complete Guide to Audit Requirements Worldwide (2026)”, “description”: “A comprehensive guide to mandatory audit thresholds, regulatory bodies, and compliance deadlines across major jurisdictions including US, UK, EU, and Australia.”, “image”: “https://bato.com.np/assets/images/audit-guide-cover.jpg”, “datePublished”: “2026-02-16”, “dateModified”: “2026-02-21”, “author”: { “@type”: “Person”, “name”: “Senior Audit Editor” }, “publisher”: { “@type”: “Organization”, “name”: “BATO - Business Audit & Tax Organization”, “logo”: { “@type”: “ImageObject”, “url”: “https://bato.com.np/assets/images/logo.png” } } } ] }

Navigating the global landscape of statutory audit obligations is essential for CFOs, controllers, and company secretaries managing multi-jurisdictional entities. This guide covers mandatory audit thresholds across major economies, the international audit standards hierarchy, and how to prepare your organization for a smooth audit.

What is a Statutory Audit?

A statutory audit is a legally mandated review of a company’s financial statements conducted by an independent, licensed auditor. Unlike internal audits (which serve management), statutory audits are designed to give external stakeholders — shareholders, creditors, regulators — confidence in the accuracy and fairness of reported financial information.

The auditor’s opinion takes one of four forms:

- Unqualified (clean) opinion — financial statements present fairly in all material respects

- Qualified opinion — material misstatement in a specific area, but rest is fair

- Adverse opinion — financial statements are materially misstated

- Disclaimer of opinion — auditor unable to obtain sufficient evidence

Statutory Audit Thresholds by Jurisdiction

United Kingdom

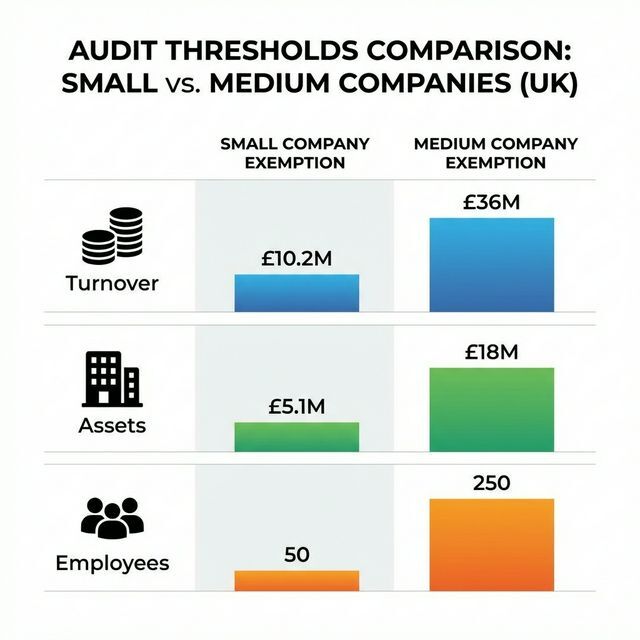

UK companies are exempt from audit if classified as a “small company” — meeting at least 2 of 3 criteria in the current and prior year:

| Criterion | Threshold |

|---|---|

| Annual turnover | ≤ £10.2 million |

| Balance sheet total | ≤ £5.1 million |

| Average employees | ≤ 50 |

Important exceptions: Public companies, banking or insurance companies, subsidiaries of groups that do not qualify as small at group level, and companies that are in their first year (automatic audit exemption in year 1 does not apply universally) — all require audits regardless of size.

UK auditing is overseen by the Financial Reporting Council (FRC) and implemented by registered auditors under ISAs (UK).

European Union

The EU Accounting Directive sets minimum criteria but allows member states to apply lower thresholds. Companies exceeding at least 2 of 3 criteria must have a statutory audit:

| Country | Turnover | Assets | Employees |

|---|---|---|---|

| Germany | > €12M | > €6M | > 50 |

| France | > €8M | > €4M | > 50 |

| Netherlands | > €12M | > €6M | > 50 |

| Spain | > €5.7M | > €2.85M | > 50 |

| Italy | > €8.8M | > €4.4M | > 50 |

| Poland | > PLN 5M | > PLN 2.5M | > 50 |

| Sweden | > SEK 3M | > SEK 1.5M | > 3 |

| Ireland | > €12M | > €6M | > 50 |

Listed company exception: All EU-listed companies must have a statutory audit regardless of size, conducted by a registered Statutory Auditor under EU Audit Regulation (537/2014).

United States

The US has no general federal audit requirement for private companies. However, mandatory audits apply in specific circumstances:

- SEC-registered (public) companies: Annual audit required; Big 4 or national firm required for large accelerated filers

- Federal funding recipients: Organizations receiving ≥ $750,000 in federal awards must have a Single Audit (per the Uniform Guidance / OMB A-133)

- Financial institutions: Federal banking regulators require audited financial statements for banks over $500M in assets

- Loan covenants: Most significant credit facilities require annual audited financials as a covenant

- Private equity portfolio companies: PE-backed companies typically required to deliver audited financials within 90–120 days of year end

The SEC requires PCAOB-registered firms for public company audits. The AICPA governs non-public company audit standards in the US (US GAAS).

Australia

ASIC requires large proprietary companies (those meeting 2 of 3 criteria) to prepare audited financial statements:

| Criterion | Threshold |

|---|---|

| Annual revenue | ≥ AUD $50 million |

| Total assets | ≥ AUD $25 million |

| Employees | ≥ 100 |

All registered schemes, foreign-controlled entities, and publicly listed companies in Australia require annual audits.

Canada

Public companies (reporting issuers) in Canada require annual audited financial statements filed with provincial securities regulators. The CPAB (Canadian Public Accountability Board) inspects auditors of public companies.

Private companies generally only require audits when required by lenders, investors, or debt covenants. However, co-operatives, not-for-profits over a certain size, and regulated entities (insurance companies, credit unions, pension plans) have mandatory audit requirements under sector-specific legislation.

Singapore

Companies in Singapore must be audited unless they qualify as “small companies” — satisfying at least 2 of 3 criteria:

| Criterion | Threshold |

|---|---|

| Annual revenue | ≤ SGD $10 million |

| Total assets | ≤ SGD $10 million |

| Employees | ≤ 50 |

The ACRA (Accounting and Corporate Regulatory Authority) registers public accountants permitted to conduct statutory audits.

International Audit Standards Hierarchy

Most countries (over 130) have adopted or aligned with the International Standards on Auditing (ISAs) issued by the International Auditing and Assurance Standards Board (IAASB):

Key ISA Standards

| Standard | Topic |

|---|---|

| ISA 200 | Overall objectives of the independent auditor |

| ISA 240 | Auditor’s responsibilities relating to fraud |

| ISA 260 | Communication with those charged with governance |

| ISA 315 | Identifying and assessing risks of material misstatement |

| ISA 330 | Auditor’s responses to assessed risks |

| ISA 500–580 | Audit evidence (confirmations, sampling, analytical procedures) |

| ISA 700–720 | Audit reporting (forming an opinion, comparative information, other information) |

The PCAOB (US Public Company Accounting Oversight Board) governs audits of US public companies and non-US companies listed on US exchanges, with standards that differ from IAASB ISAs in some areas.

Preparing for Your Statutory Audit

A well-prepared organization reduces audit friction and cost significantly. Key preparation steps:

1. Pre-audit reconciliations (6–8 weeks before year-end)

- Bank and investment account reconciliations complete and reviewed

- All sub-ledgers (AR, AP, fixed assets, inventory) reconciled to the general ledger

- Intercompany balances agreed and eliminated

2. Documentation assembly (year-end closing)

- Board minutes for the year

- All material contracts (leases, debt agreements, customer contracts)

- Legal letters for contingent liabilities

- Support for significant estimates (impairment analyses, warranty reserves, pension assumptions)

3. Preparing the audit readiness package

- Signed management representation letter (provided by auditor template)

- Consolidation schedules for group audits

- Related party transaction listing

4. Audit committee coordination

- Agree on audit timeline, scope, and significant accounting areas

- Review proposed adjustments before audit committee presentation

- Discuss going concern assessment if applicable

Auditor Selection and Rotation

Rotation requirements:

- EU listed companies: mandatory auditor rotation every 10 years (with possible 10-year extension if jointly tendered)

- US public companies: audit partner (not firm) rotation required every 5 years

- UK listed companies: mandatory firm rotation every 20 years (with re-tendering every 10 years)

Cost benchmarks:

- SME statutory audit: £10,000–£50,000 depending on complexity

- Mid-market company: £50,000–£300,000

- Large listed company (FTSE 250): £1M–£10M+

Related Articles

- AI in Accounting & Audit: The Practical 2026 Guide

- What is an Internal Audit? A Beginner’s Guide to Roles & Process

- Internal Audit Framework: Building an Effective Audit Function from Scratch

- Financial Statement Analysis: How to Read and Interpret Every Line

Why Audits Matter

- Credibility: Enhances trust with stakeholders.

- Compliance: Avoids legal penalties.

- Insight: Identifies internal control weaknesses.

Audit Thresholds by Jurisdiction

United Kingdom (UK)

In the UK, a company is generally exempt from audit if it qualifies as a “small company.” To qualify, it must meet at least two of the following checks:

- Turnover: Not more than £10.2 million

- Balance Sheet Total: Not more than £5.1 million

- Employees: Not more than 50 employees

European Union (EU)

The EU sets baseline criteria, but individual member states can set their own.

Germany

- Turnover: > €12 million

- Total Assets: > €6 million

- Employees: > 50

France

- Turnover: > €8 million

- Total Assets: > €4 million

- Employees: > 50

United States (USA)

Unlike many other countries, the US does not have a federal requirement for all private companies to be audited. However, audits are required for:

- Publicly traded companies (SEC requirements).

- Companies receiving significant federal funding.

- Private companies with specific loan covenants or investor requirements.

Australia

ASIC requires large proprietary companies/entities to prepare and lodge audited financial reports. A proprietary company is ‘large’ if it satisfies at least two of the following criteria:

- Revenue: $50 million or more

- Assets: $25 million or more

- Employees: 100 or more

International Standards on Auditing (ISA)

Most countries (over 130) have adopted the International Standards on Auditing (ISA) issued by the IAASB.

Key Standards

- ISA 200: Overall Objectives of the Independent Auditor

- ISA 315: Identifying and Assessing the Risks of Material Misstatement

- ISA 700: Forming an Opinion and Reporting on Financial Statements

Preparing for Your Audit

- Reconcile Accounts: Ensure all bank and sub-ledger accounts reconcile to the general ledger.

- Gather Evidence: Have invoices, contracts, and board minutes ready.

- Review Controls: Document internal controls and processes.

Conclusion

Understanding your audit obligations is the first step towards global compliance. Failure to comply can result in severe fines and reputational damage.