Series A Fundraising: Complete Guide to Venture Capital Financing, Due Diligence, and Investment Terms (2026)

Series A represents the critical transition from seed-stage survival to growth-stage scaling. This guide covers the complete Series A fundraising process.

Series A Overview

Fundraising Fundamentals

Series A Landscape (2026):

Market Dynamics:

Total US VC Investment: $80B+/year (2024-2026 range)

Median Series A Size: $4-8M

Median Series A Valuation: $10-25M post-money

Expected Use of Funds (Typical allocation):

- Product development: 35-45%

- Sales & marketing: 25-35%

- Operations/admin: 15-25%

- Contingency/working capital: 5-10%

Example $5M raise use:

- Product team (engineering): $1.75M

- Sales/marketing/go-to-market: $1.5M

- Operations (finance, HR, legal): $0.75M

- Contingency: $0.25M

Runway Created:

- Monthly burn to achieve: $1.2M (estimated)

- $5M provides: ~4 years runway (if well-managed)

- Expectation: Profitability or next raise within 3-4 years

Investor Types:

Micro-VCs ($50M-$500M under management):

- Check sizes: $250K-$1M

- Often lead smaller Series A rounds

- More engaged mentoring

- Focus: Specific niches/geographies

Traditional VCs ($500M-$3B+ under management):

- Check sizes: $1M-$5M+

- Can lead larger Series A rounds

- Institutional backing

- Examples: Sequoia, Andreessen Horowitz, Accel

Corporate Venture Arms:

- Check sizes: Varies ($500K-$5M+)

- Strategic alignment expectations

- May involve product partnerships

Timeline Expectations:

Pitch to close: 6-9 months typical

- Month 1-2: Pitch process, warm introductions

- Month 2-4: Due diligence

- Month 4-6: Term sheet negotiation

- Month 6-9: Legal closing/documentation

Fast-tracked (exceptional deal): 3-4 months

- Strong traction

- Low legal/IP complexity

- Competitive process (multiple offers)

Slow process (complicated): 12+ months

- Novel/complex IP

- International regulatory issues

- Competitive pressure low

Valuation Benchmarks (2026):

By Maturity/Traction:

- Seed revenue ($0-$100K ARR): $5-15M valuation

- Early traction ($100K-$500K ARR): $15-40M

- Strong traction ($500K-$2M ARR): $40-100M

- Exceptional ($2M+ ARR): $100M+ (unicorn path)

Example: SaaS company

- $500K ARR (strong for Series A)

- Benchmark: 10-15x revenue multiples

- Implied valuation: $5-7.5M

- But: Market opportunity, growth rate, team drive actual valuation

- Actual Series A likely: $20-40M (expectation of 10x growth)

Capital Sources Beyond VC:

Venture debt: $500K-$2M

- Lower dilution than equity

- Repaid from future revenue/equity raise

- Cost: 8-15% interest + warrant coverage (0.5-1.5%)

- Extends runway without dilution

- Example: $1M Series A + $500K venture debt = $1.5M total available

Grants/non-dilutive funding: Up to $500K

- SBIR grants: $150K-$1M

- Industry grants/competitions

- No dilution to founders

- 6-12 month timelines

- Typical: Cover specific R&D projects

Strategic partnerships: Variable

- Customer prepayments

- Partnership revenue

- Not typical to rely on

Total Series A capital: Equity (mostly) + Debt (optional) + Grants/partnerships

The Fundraising Process

Investor Research and Outreach

Identifying Target Investors:

Investor Sourcing:

Primary Sources:

1. Warm introductions (Most effective, 40-60% response rate)

- Board members/advisors connecting you

- Prior investors introducing

- Other founders referring

- Highest quality - investors predisposed

2. Cold outreach via email/LinkedIn (10-20% response rate)

- Personalized pitches (not blast emails)

- To specific investment theses matching company

- Reference partner focus areas

- Lower conversion but accessible

3. Conferences/events (20-30% response rate)

- Demo days (Pitch competitions)

- Industry conferences (relevant sector events)

- VC-specific conferences

- Face-to-face interaction valuable

4. Venture databases

- Crunchbase, PitchBook, AngelList

- Research investor focus areas

- Identify warm connections

- Research recent investments

Investor Evaluation Framework:

Criteria for Target Investors:

✓ Check size matches needs ($1M+ for Series A lead)

✓ Geographic focus (or remote-friendly)

✓ Sector expertise (your industry/space)

✓ Stage focus (Series A emphasis, not mega-late stage)

✓ Value-add beyond capital (connections, credibility)

✓ Portfolio reputation (reference ability)

✓ Lead investor vs. follower (who'll drive round)

Red Flags:

✗ Unclear investment criteria

✗ No prior exits or portfolio companies

✗ Pressure to close quickly without due diligence

✗ Founder stories of difficult post-investment relationship

✗ Minimum ownership requirement (>20% at Series A usually)

✗ Heavy-handed board involvement expectations

✗ Bad reputation in founder community

Reference Checks:

- Contact prior portfolio founders

- Ask about: Responsiveness, board dynamics, helpful advice, fundraising support, down-round handling

- Build picture of partner relationship quality

Building Investor List:

Target List Size: 30-50 investors

- Top tier (dream investors): 10-15

- Secondary tier (good fit): 15-20

- Backup tier (fallback): 5-10

Targeting Strategy:

- Reach out in waves (not all at once)

- Wave 1: 15-20 top investors (4-week window)

- Wave 2: Additional 20-30 if needed (after feedback)

- Avoid: Blasting all at once (signals lack of targeting)

Sequencing Logic:

- Start with less-obvious investors (get feedback/practice)

- Move to tier-1 investors after refining pitch

- Leave some investors for end (backup options)

- Test messaging with friendly advisors first

Pitch and Presentation

Crafting a Winning Pitch:

Pitch Deck Structure (10-15 slides typical):

1. Cover Slide (1)

- Company name/logo

- One-liner: What you do (simple customer language)

- Founder names/titles

- Contact info

2. Problem Slide (1)

- What problem are you solving?

- Show data/statistics

- Make problem visceral (why should investor care?)

Example Problem:

"Enterprise document management: Companies spend $15K+/year

on outdated doc management. Process improvement is critical,

affecting compliance, security, and productivity.

Market size: $50B+ annual spend."

3. Solution Slide (1)

- Your solution (simple, clear)

- Key differentiators

- Why you're better than alternatives

Example:

"DocFlow: AI-powered document management cutting

time-to-document 80%, with enterprise security.

Differentiator: Plug-and-play (vs. 6-month implementations)"

4. Market Size Slide (1)

- Total addressable market (TAM)

- Serviceable addressable market (SAM)

- Serviceable obtainable market (SOM)

Example:

TAM: $50B global document management

SAM: $8B enterprise SaaS in US

SOM: $200M achievable (year 5 goal)

5. Business Model Slide (1)

- How do you make money?

- Pricing model

- Unit economics preview

Example:

"SaaS model: $2K-$20K/month depending on usage

Target: 40%+ gross margin year 1, 70%+ year 3"

6. Traction Slide (1-2)

[Most important for investors]

- Revenue/ARR to date

- Customer growth

- User metrics

- Partnerships

Example:

"Current: $300K ARR, 25 customers, 40% month-over-month growth

Trajectory: $1.2M ARR projected year-end (20-customer cohort)"

7. Team Slide (1)

- Key team members

- Relevant background

- Why this team can execute

Example:

CEO: 10 years enterprise software, prior company sold to Google

CTO: ML engineer from major SaaS company

VP Sales: Former AWS account executive

8. Financials/Unit Economics (1-2)

- Revenue model clarity

- LTV/CAC ratio

- Path to profitability

Example:

CAC: $15K (average to acquire customer)

LTV: $120K (3-year customer value)

LTV/CAC: 8x (excellent, >3x healthy)

Payback: 15 months

9. Use of Funds (1)

- How you'll use $5M

- Hiring plan (what positions)

- Milestones achievable

Example:

"Product/Engineering: $1.75M (5 engineers)

Sales/Marketing: $1.5M (2 AEs, 1 marketing manager)

Operations: $0.75M (CFO, HR, Finance)

Contingency: $0.25M

Runway: 48 months to profitability target"

10. Why Us / Competition Slide (1)

- Why your team/product

- Competitive landscape

- Sustainable differentiation

Example:

"Proprietary ML models (18-month head start)

Enterprise trust (partnerships with Salesforce, Microsoft)

Market timing (AI adoption accelerating 2025-2026)"

11. Ask/Investment Summary (1)

- Amount raising

- Note on led vs. oversubscribed

- Key milestones post-investment

Example:

"Raising $5M Series A

$2M already committed, seeking lead investor

Milestones: $750K ARR by month 18, profitability by month 36"

Pitch Deck Design:

- Clean, professional template (not cluttered)

- Consistent branding

- Data visualization (not walls of text)

- 10-15 slides (not 50)

- Speaking notes (for you, not on slides)

Elevator Pitch (30 seconds):

Develop concise 30-second version:

"We're building the AI-powered document management system

for enterprise. Companies spend $15K+ annually, but process

is broken. We've got 25 customers today paying $2K-$20K/month,

growing 40% month-over-month. We're raising $5M to scale the

sales team and hit profitability in 36 months."

Pitch Delivery Tips:

✓ Practice extensively (20+ times before pitching VCs)

✓ Know deck cold (practice without slides)

✓ Tell story, not lecture

✓ Emphasize traction (investors believe metrics)

✓ Be authentic (VCs smell BS)

✓ Ask for money (be direct about ask)

✓ Expect pushback (don't be defensive)

✓ Keep meetings to 60 minutes (respect time)

Due Diligence Process

What VCs Will Investigate

Comprehensive Due Diligence:

Financial Due Diligence:

What VCs Verify:

1. Historical financials

- Revenue accuracy (contracts, receipts)

- Expense tracking (real costs)

- Burn rate calculation

- Cash runway

2. Financial model

- Assumptions documented

- Revenue projections conservative

- Expense forecasts realistic

- Path to profitability clear

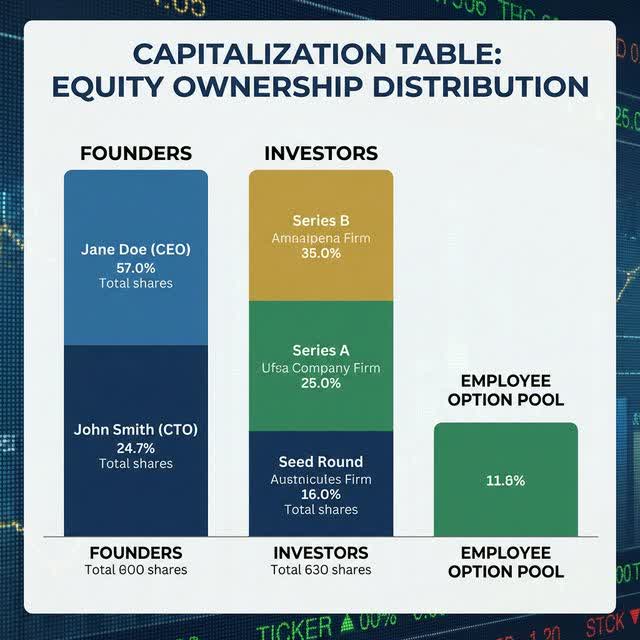

3. Cap table accuracy (see our [comprehensive cap table management guide](/2026-02-19-cap-table-management-guide/))

- All shares documented

- 409A valuations current

- No equity disputes

- Fully-diluted shares correct (including [equity compensation grants](/2026-02-19-equity-compensation-stock-options-guide/))

4. Unit economics

- CAC calculation (customer acquisition cost)

- LTV calculation (lifetime value)

- LTV/CAC ratio (3x+ healthy)

- Payback period (<18 months healthy)

- Gross margins (30%+ minimum for SaaS)

Documentation Required:

- 3 years historical P&L

- Monthly financials (last 12 months)

- Balance sheet (current)

- Cash flow statement

- Customer contracts (sample)

- Pricing/packaging documentation

- Salary schedules

- Stock option plan documentation

Red Flags:

✗ Inconsistent financial statements

✗ Unaccounted cash (missing revenue sources)

✗ Unit economics don't make sense

✗ No clear path to profitability

✗ CAC/LTV ratio < 3x (unit economics broken)

Technical Due Diligence:

What VCs Check:

1. Product

- Functionality demonstrations

- Tech stack evaluation

- Scalability assessment

- Security posture

- IP ownership documentation

- Patent filing strategy

2. Engineering team

- Code review (sample)

- Development processes

- DevOps/deployment

- Testing practices

3. Intellectual property

- Founders assigned IP (written agreements)

- No competitor/vendor IP used

- Patent landscape reviewed

- Trademark/branding secured

- Code licensing reviewed (no GPL/viral licenses causing issues)

4. Data/Security

- Data protection practices

- Encryption standards

- Compliance (GDPR, CCPA, HIPAA as relevant)

- Third-party security audit

- Data backup/disaster recovery

Documentation Required:

- IP assignment agreements (founders → company)

- Code repository access (for review)

- System architecture diagrams

- Security audit results

- Compliance certifications

- Product roadmap (3-year vision)

Legal Due Diligence:

What VCs Verify:

1. Company formation

- Articles of incorporation

- Bylaws

- Good standing status

- Board resolutions (all major decisions)

2. Equity/cap table

- Stock records (books and records)

- All options documented

- Ed board resolutions

- Founder agreements

- Employee option grants

3. Contracts/agreements

- Material customer contracts

- Vendor agreements

- Employment agreements

- Confidentiality/IP assignment

- Non-compete review

4. Litigation/compliance

- No ongoing lawsuits

- Import/export compliance

- Tax status (current filings)

- Regulatory compliance

- License status (business, professional)

Documentation Required:

- Certificate of good standing

- Articles/bylaws

- Board meeting minutes (all significant decisions)

- Stock ledger (shares issued, dates)

- Cap table (as above, multiple reviews)

- Key contracts (redacted if needed)

- Employment agreements

- Option grants and plan

- Insurance policies

- Compliance documentation

Customer/Market Due Diligence:

What VCs Verify:

1. Customer validation

- Reference calls (5-10 customers)

- Churn rate (customer retention)

- NPS/satisfaction data

- Customer concentration (top 5 customers = <30% revenue)

- Product-market fit signals

2. Market opportunity

- TAM reassessed

- Competitive landscape evaluated

- Go-to-market strategy feasible

- Sales pipeline quality

3. Management team

- Background verification

- Reference calls (prior employers)

- Completeness (any critical hires missing?)

- Founder commitment (full-time, not side projects)

Documents/Access Needed:

- Customer reference list

- Sales pipeline/opportunity stage

- Customer agreements

- NPS survey results

- Churn analysis

- Competitive analysis

- Management team backgrounds

Common Deal Killers:

Issues that end funding:

✗ Founder misrepresentation (lying about revenue, users)

✗ Co-founder disputes (pending litigation over equity)

✗ Undisclosed IP claims (prior employer claiming code ownership)

✗ Broken unit economics (path to profitability doesn't work)

✗ Massive customer concentration (one customer = 50%+ revenue)

✗ Key person risk (only founder can operate product)

✗ Regulatory red flags (unlicensed activities)

✗ Major security breach (exposed customer data)

✗ Abandoned cap table (too many disputed shareholders)

Term Sheet and Closing

Understanding Key Terms

Series A Term Sheet Fundamentals:

Term Sheet Overview:

Document: Non-binding (mostly) outline of investment terms

Parties: Investor(s), Company founders

Purpose: Align on key terms before legal documentation

Timeline: Negotiation typically 2-4 weeks

Key Sections:

1. Investment Structure

- Amount: $5M (example)

- Security: Series A Preferred Stock

- Price per share: $2.00 (calculated from valuation)

- # of shares: $5M / $2.00 = 2.5M shares

- Investor ownership: 2.5M / (7.5M fully-diluted) = 33%

2. Valuation

- Pre-money: $15M (implied by price)

- Post-money: $20M ($15M + $5M raised)

- Investor ownership: $5M / $20M = 25% post

- Founder dilution: From ~70% (seed) → 52.5% post

3. Liquidation Preference

- 1x non-participating preferred (standard)

- OR: 1x participating preferred (unfavorable to founders)

- Meaning: Investor gets $5M back before common shareholders

1x non-participating definition:

- In liquidity event, investor gets amount invested

- Then pro-rata participation with common if more cash available

- Can't double-dip (takes either pref or pro-rata, not both)

4. Anti-Dilution

- Weighted-average (most common, founder-friendly)

- Full ratchet (rare, founder-hostile)

- Carve-out (for employee options issued)

5. Investor Rights

- Board seat (investor appoints director)

- Information rights (quarterly financials, cap table)

- Pro-rata rights (can participate in future rounds)

- Drag-along rights (can force minority in acquisition)

- Anti-dilution (as above)

6. Protective Provisions

- Investor veto on: Buying/selling company, issuing new stock,

Changing cap table, Related party transactions, New debt

- Prevents founders from diluting investor without approval

7. Representations and Warranties

- Company statements about itself

- Founder liability exposure

- Example: "No undisclosed litigation, IP properly owned, financials accurate"

8. Conditions to Closing

- 409A valuation completed

- Cap table clean (no disputes)

- No material adverse changes

- Founder agreements signed

- Legal documents executed

Valuation Negotiation:

Common Starting Points:

- Founder expectation: More optimistic valuation

- Investor expectation: More conservative valuation

- Gap: Often 20-40% difference initially

- Goal: Negotiate to middle ground acceptable to both

Factors Influencing Valuation:

Upside:

✓ Strong revenue traction (most important)

✓ Explosive growth rate (month-over-month)

✓ Large TAM (market opportunity)

✓ Experienced team (execute risk lower)

✓ Novel IP/technology (defensibility)

✓ Competitive process (multiple offers)

Downside:

✗ Early-stage (pre-revenue or minimal)

✗ Unknown market (unproven demand)

✗ Weak team (execution risk)

✗ Commodity product (no differentiation)

✗ Limited traction (slow growth)

✗ Competitive product (me-too risk)

Typical Valuation Ranges (2026):

Seed-Stage Pre-Series A: $3-10M

- Pre-revenue/minimal traction

- Experienced founder(s)

- Clear opportunity

Series A Strong Traction: $15-50M

- $200K-$1M ARR

- Monthly growth 20-40%

- Product-market fit signals

- Strong team

Series A Exceptional: $50M-$100M+

- $1M+ ARR

- 50%+ monthly growth

- Clear unicorn trajectory

- Multiple term sheets

Negotiating the Valuation:

Founder Strategy:

1. Research comparables

- Similar companies raises

- Reports from CB Insights, Crunchbase

- Industry benchmarks

2. Build tension

- Multiple investors interested (generate competition)

- One term sheet increases leverage

- Strategic alternatives (venture debt, slower growth, partnership)

3. Separate points

- If investor firm on $20M valuation

- Negotiate other terms more favorable

- Lower preference (e.g., 0.75x instead of 1x)

- Remove/limit anti-dilution

- Pro-rata rights (founder friendly)

4. Walk away option

- Willingness to turn down bad deal

- Signals strength in negotiation

- Venture debt + slower growth alternative

- Avoid desperation

Investor Negotiation Points:

Typical Investor Asks:

- Board seat (standard)

- Information rights (standard)

- Pro-rata rights (standard)

- Anti-dilution (standard)

- Liquidation preference (1x standard, 1x non-part standard)

- Key-person insurance (for founder retention)

- Founder vesting acceleration (cliff completion triggers bonus equity)

Avoid Accepting:

✗ Liquidation preference > 1x (participating is worse)

✗ Full-ratchet anti-dilution (weighted-average standard)

✗ No pro-rata founder participation in future rounds

✗ Drag-along rights (force sale of company) without investor drag-along reciprocal

✗ Excessive protective provisions (investor veto on minor decisions)

✗ Minimum ownership requirements (>15% typically unreasonable)

✗ Redemption rights (investor can force buyback later)

Post-Series A: Execution and Growth

Post-Funding Priorities:

First 30 Days Post-Close:

Priority 1: Capitalize on momentum

- Announce funding (press release, social media)

- Customer communications (new product roadmap)

- Team announcement (new hires planned)

- Build confidence (seed/Series A investors, customers)

Priority 2: Hire aggressively

- Fill critical roles planned (sales, engineering)

- Timing: Market opportunity exists now

- Speed: Hires can impact year-end targets

- Quality: Don't drop bar (hiring best matters)

Priority 3: Monthly board meetings

- First board meeting within 20 days

- Set cadence (monthly typical)

- Prepare materials (dashboard, challenges, asks)

- Establish rituals (executive updates, metrics review)

Metrics to Track (Board Dashboard):

Financial:

- Monthly recurring revenue (MRR) / Annual recurring revenue (ARR)

- Monthly growth rate

- Burn rate

- Cash runway

- CAC (customer acquisition cost)

- LTV (lifetime value)

- Gross margin

Operational:

- Active customers (count)

- Churn rate (monthly)

- Sales pipeline ($ value, conversion)

- Headcount (plan vs. actual)

- Product development progress (features shipped)

- Key partnership milestones

Strategic:

- Competitive wins (vs. whom, why)

- Market expansion (new segments, geographies)

- Product-market fit evidence

- Path to Series B clarity (18-month outlook)

Board Priorities (Year 1):

Targets for Board Success:

- Revenue: 3-5x ARR growth (from Series A close)

- Growth rate: Maintain 20-30% month-over-month

- Unit economics: Improve CAC/LTV ratio

- Hiring: Complete hiring plan (or >80% of plan)

- Product: Ship major product roadmap items

- Market: Establish category leadership (in segment)

Milestones to Hit:

- Month 6: Halfway to year revenue target

- Month 12: Hit $X ARR target (agreed pre-funding)

- Month 18: Be prepared to raise Series B

- Month 24: Show path to profitability or massive growth opportunity

Series B Preparation (Months 12-18):

Parallel to Execution:

- Continue business building (don't stall for fundraising)

- Begin investor research (12-18 months before Series B desired)

- Prepare metrics for Series B (run clean financials)

- Team building (add board-caliber executives for Series B)

Series B Expectations:

- Revenue: $3-5M+ ARR (benchmark)

- Growth: 15-25% monthly growth

- Unit economics: Proven (CAC/LTV > 3x, efficient growth)

- Team: VP-caliber in major functions

- Product: Clear market leadership in segment

- Traction: Clear path to Series C/IPO

Conclusion

Series A fundraising is a critical milestone requiring careful planning, diligent execution, and negotiation skills. Key success factors:

- Build genuine traction - Revenue and growth metrics drive valuation

- Prepare thoroughly - Due diligence readiness prevents deal delays

- Know your numbers - Valuation range, unit economics, financials

- Build relationships - Warm introductions and investor fit matter

- Negotiate from strength - Competitive process, alternatives strengthen your position

- Maintain focus post-funding - Execution matters more than capital

- Plan for Series B - Build metrics from day 1 of Series A capital use

Frequently Asked Questions

Q: Should I raise Series A now or wait for more traction?

A: General rule: Raise when you have 6-12 months of runway remaining AND clear evidence of traction (revenue, growth, or user adoption). Waiting for “perfect” metrics delays capital access; raising too early wastes time on fundraising with weak metrics. Optimal: 3-6 months revenue history showing 20%+ monthly growth, 500+ users, or $5-10K MRR.

Q: What’s the typical VC due diligence process and timeline?

A: Due diligence typically follows this timeline: (1) Initial term sheet offer (non-binding); (2) Technical/legal due diligence (2-3 weeks)—investor hires lawyers/accountants to review; (3) Commercial due diligence (2-4 weeks)—investor calls customers, reference checks; (4) Final sign-offs (1-2 weeks); (5) Legal documentation and closing (2-4 weeks). Total typically 4-8 weeks from LOI to funding.

Q: What happens if I get multiple term sheets?

A: Multiple term sheets create competitive tension, strengthening your negotiating position. You can: (1) Use best offer to improve terms with other investors; (2) Ask investors for “final offers” within deadline; (3) Negotiate sequentially downward through offers; (4) Ask investors if they’ll match better terms. Typical practice: Tell investors you’re in process with others, create slight urgency, negotiate best final terms, then pick best investor relationship (not always highest valuation).

Q: Should I hire a lawyer before approaching Series A investors?

A: Yes. Hire venture-stage corporate counsel (law firm with VC experience) to review cap table, incorporation docs, and advise on fundraising process. Cost: $5-15K for setup and early guidance. This resolves cap table issues, IP ownership, and securities law compliance BEFORE investor due diligence. Lawyer selected also handles legal documentation during closing ($15-30K additional).

Q: What if I disagree with investor projections expectations?

A: Your 3-5 year projections should be credible but optimistic (30-50% growth in early years realistic for high-growth startups). If investor questions your projections as unrealistic: (1) Justify with customer pipeline data; (2) Show historical growth rates; (3) Break down customer acquisition and expansion assumptions. Conservative projections are safer; overly aggressive projections suggest founder doesn’t understand market realities.

Q: Can I negotiate employee equity pool size with Series A investors?

A: Yes, but expect pushback. Typical: 10-20% fully-diluted equity reserved for options. Investors want room for future hiring without excessive dilution. Negotiate: (1) New employee pool size (5-10k shares typical for small company); (2) Vesting schedule (4-year standard with 1-year cliff); (3) Exercise price (strike price at ISO tax-favorable levels). If you need larger pool for headcount plans, justify with hiring roadmap.

Q: What metrics should I track for Series A due diligence?

A: Essential metrics: Monthly revenue (and trend), MAU/DAU (monthly/daily active users), NRR (net revenue retention), churn rate, CAC (customer acquisition cost), LTV (lifetime value), burn rate, gross margin (if applicable). These metrics demonstrate product-market fit and efficient growth. Most investors request 4-year projections; prepare multiple scenarios (base case, upside, downside).

Q: How do liquidation preferences work if company is acquired?

A: Liquidation preference determines payout order in acquisition. Standard: Series A investors get 1x preference (get money back before common stockholders). Example: $10M acquisition, $5M Series A preferred with 1x preference = Series A investors paid $5M, common shareholders split remaining $5M. Non-participating preference (standard) means investors don’t also participate in remaining proceeds after 1x returned.

Q: What’s the difference between SAFE notes and Series A priced rounds?

A: SAFE (Simple Agreement for Future Equity) is a short-term note converting to equity in a future priced round (no interest/maturity date). SAFE is quicker, simpler, but doesn’t establish valuation or investor rights. Series A is priced round establishing valuation, governance rights, liquidation preferences. SAFE typically used for seed rounds; Series A for post-product-market-fit companies. SAFE delays valuation; Series A establishes it.

Q: Can I negotiate the board seat with my Series A investor?

A: Yes. Board composition is standard negotiation point. Typical: 3-person board (founder as CEO/chair, non-founder investor director, independent director). Investor expects board seat; you negotiate: (1) Which investor gets seat (lead investor standard); (2) Board size (3 vs. 5 seat boards); (3) Whether investor forced to have independent director. Board seat gives investor influence but also liability/fiduciary duties.

Resources

- Crunchbase: Investor database and funding news

- PitchBook: VC/private equity term sheet data and market trends

- AngelList: Investors, job board, cap table tools

- NVCA Term Sheet: Standard Series A term sheet template

- Ledgy: Cap table and documentation management

- YCombinator Resources: Startup resources and guides

- Venture Capital Law: VC law resources and templates

Related Articles

- Series A Term Sheet Negotiation: Key Clauses Founders Must Understand

- Venture Capital Term Sheets: Complete Guide to Key Terms, Negotiation Tactics, and Founder Protection (2026)

- Private Equity vs Venture Capital: How They Actually Differ

- Venture Debt Explained: When and How Startups Should Use It

- How to Prepare for a Series B Financial Audit: The Founder’s Checklist