Startup Equity 101: A Founder's Guide to Stock Options and Vesting

Startup equity is one of the most powerful wealth-creation tools in modern capitalism — and one of the least understood. Founders grant options to employees without fully explaining what they mean. Early employees accept equity packages without knowing how to evaluate them. First-time founders set up their cap tables in ways that will haunt them through every subsequent fundraise.

This guide demystifies startup equity from the ground up — whether you are a founder designing your first option plan or an employee evaluating a job offer at a Series B startup.

How Startup Equity Works: The Basics

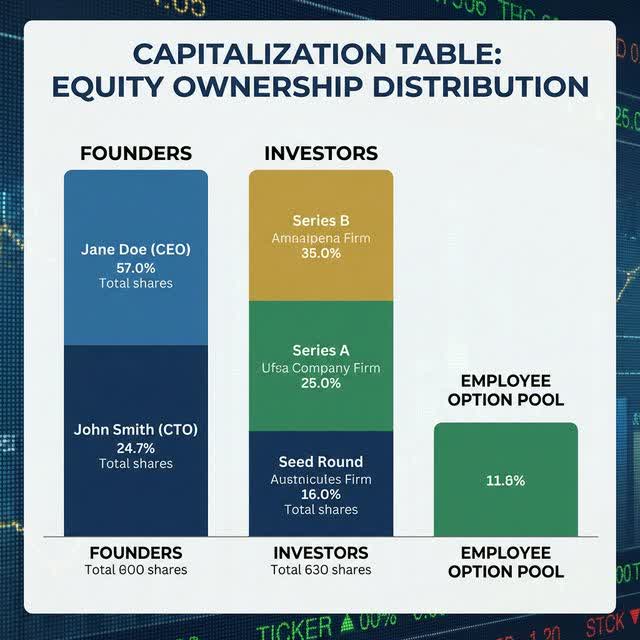

When you found a startup and incorporate, you and your co-founders divide the initial shares between you — typically several million shares at a fraction of a cent each (the par value). These are your common shares.

When you raise money from investors, you typically issue preferred shares — a senior class of stock with special rights (liquidation preference, anti-dilution protection) that protect investors in downside scenarios. This is a critical distinction captured in your cap table.

Employees receive neither of these. They receive stock options — the right to purchase common shares in the future at a fixed price.

Stock Options: ISOs vs NSOs

All employee stock options are either Incentive Stock Options (ISOs) or Non-Qualified Stock Options (NSOs). The tax consequences differ dramatically:

| Feature | ISOs | NSOs |

|---|---|---|

| Who can receive them | Employees only | Employees, advisors, board members |

| Tax at grant | None | None |

| Tax at exercise | None (AMT may apply) | Ordinary income tax on spread |

| Tax at sale | Capital gains | Capital gains on appreciation post-exercise |

| Annual ISO limit | $100K per year | No limit |

For most employees, receiving ISOs is significantly more favorable. The tax is deferred until sale, at which point capital gains rates (20% at the federal level) apply rather than ordinary income rates (up to 37%).

Vesting: Why You Have to “Earn” Your Equity

Options are not granted fully on day one — they vest over time to create a retention incentive. The universal startup standard is a 4-year vesting schedule with a 1-year cliff:

- Month 1–11: No shares vest. If you leave in month 10, you receive nothing.

- Month 12 (The Cliff): 25% of your total grant vests in a single event.

- Months 13–48: The remaining 75% vests monthly (1/36 per month).

Founder Vesting: Most VCs will insist that founders also subject their shares to a vesting schedule, typically starting from the last time they took outside capital. This aligns incentives and prevents a co-founder from quitting on day 90 and retaining a massive equity stake.

The 409A Valuation: Setting the Strike Price

The exercise price of stock options must equal or exceed the Fair Market Value (FMV) of the company’s common shares as determined by an independent 409A valuation. Granting options below FMV is a serious IRS violation that creates immediate, punitive tax liability for the recipient — not the company.

Every startup should obtain a fresh 409A from a qualified firm:

- Before its first option grants.

- After every equity financing round (because the preferred stock price implies a new common stock FMV).

- At least every 12 months if no financing occurs.

Dilution: What Happens to Your Ownership Each Round

When you raise a $5M Series A and issue $5M worth of new preferred shares, all existing shareholders get diluted. If you owned 60% of the company before the round and the investors receive 20% of the company, your new ownership is approximately 48% (assuming a straight pro-rata dilution model).

But consider the math: if the pre-money valuation was $20M, your 60% stake was worth $12M. After the round (post-money valuation $25M), your 48% is worth $12M — exactly the same. The dilution in percentage was offset by an increase in per-share value.

The time to be concerned about dilution is when you are raising at a flat or down valuation — every point of dilution is destroying dollar value, not creating it.

The Option Pool Shuffle: A Key Negotiation Point

Before a funding round, VCs will often require you to expand the employee stock option pool. The critical negotiation: whether the option pool expansion happens pre-money (diluting founders before the round closes) or post-money (diluting all shareholders after the round).

Standard venture practice is pre-money option pool expansion — which means the dilution falls almost entirely on founders. Understanding the option pool shuffle is one of the most important term sheet negotiation concepts for first-time founders.

What Happens to Your Options When You Leave

For most standard option grants, departing employees have a 90-day post-termination exercise window to exercise their vested options. After 90 days, the options expire worthless.

This creates a painful dilemma: if you have 100,000 vested options with a $1.00 exercise price, exercising them costs $100,000 — money most employees cannot access without an immediate liquidity event. Additionally, early exercise of ISOs may trigger the Alternative Minimum Tax (AMT).

Some employee-friendly companies (Stripe, Lyft, and others have done this) extend exercise windows to 5 or 10 years post-departure, giving employees far more flexibility.

Conclusion

Understanding startup equity is not optional — it is a fundamental financial literacy requirement for anyone building or joining a venture-backed company. Founders who clearly and accurately communicate the value and mechanics of equity packages attract better talent. Employees who understand dilution, strike prices, and tax consequences make better decisions about when to exercise, when to hold, and when to negotiate for better terms.

Related Articles

- Equity Compensation and Stock Options: Complete Guide to Grants, Vesting, Taxation, and Accounting (2026)

- 409A Valuation: The Startup Founder’s Definitive Guide (2026)

- How to Prepare for a Series B Financial Audit: The Founder’s Checklist

- Private Equity vs Venture Capital: How They Actually Differ

Frequently Asked Questions (FAQ)

What is a stock option?

The right, but not the obligation, to purchase company shares at a fixed exercise price for a defined period. Options only have value if the current share price exceeds the exercise price.

What is the difference between ISOs and NSOs?

ISOs are for employees only and have preferential tax treatment (no ordinary income tax at exercise). NSOs can go to anyone but trigger ordinary income tax on the spread at exercise.

What is a 4-year vest with 1-year cliff?

The standard startup vesting schedule. No shares vest until 12 months (the cliff), then 25% vests at once, and the remaining 75% vests monthly over 3 more years.

What is a 409A valuation?

An independent appraisal of the company’s common stock fair market value, required so options can be priced at FMV. Must be refreshed after every financing round.

What does ‘dilution’ mean for founders?

Issuing new shares reduces existing shareholders’ percentage ownership. However, if the share price increases proportionally, total dollar value may remain the same or increase.

What is an Option Pool?

A block of shares reserved for employee equity grants. VCs typically require pool expansion before (not after) a round, meaning founders bear the dilution, not new investors.

What happens to my stock options if I leave a startup?

You typically have 90 days to exercise vested options before they expire. If you cannot afford to exercise, you forfeit the options.

What is an early exercise election (Section 83(b))?

Exercising unvested options immediately and electing to pay tax at the current (low) value now. Must be filed with the IRS within 30 days of exercise — the deadline is absolute.

What is a secondary sale of startup stock?

Selling existing shares to a third-party buyer before an IPO. Subject to company right-of-first-refusal and usually requires company permission.

What is a SAFE note?

Simple Agreement for Future Equity — a convertible instrument with no maturity date or interest, commonly used in pre-seed rounds. Converts into equity at the next priced round at a discount.